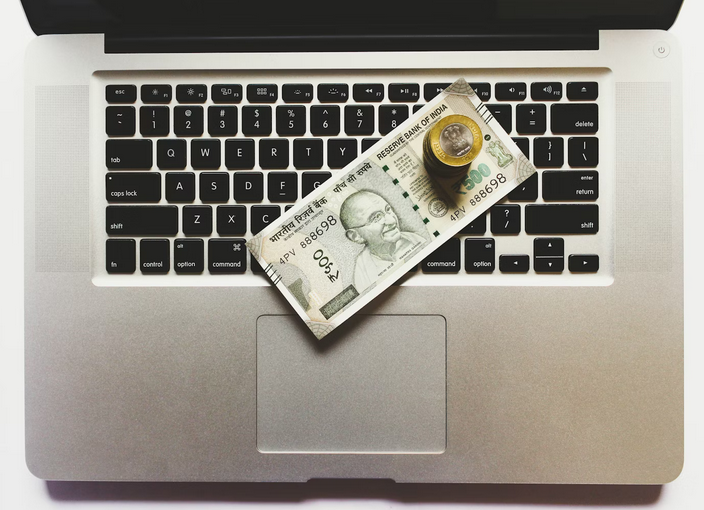

Rent is due. Your kid’s field trip fee pops up. Then your car decides it wants attention today, not next week. In such moments, Canadian Payday Loan services can look like a life jacket in choppy waters. The point is speed, not a long paperwork parade. Still, it helps to know what you’re stepping into before you click “apply.”

What an Online Payday Loan Is

An online payday loan is a small, short-term loan meant to bridge the gap until your next paycheque. It’s usually repaid in one shot on your next payday, or within a short window set by your province or territory. Think of it like borrowing a bucket to carry water across a creek, not buying a whole new plumbing system. If you need months to pay it back, this product often isn’t the right tool. In Canada, these loans are regulated mainly at the provincial and territorial level. That means the rules on maximum cost, licensing, and disclosure can vary depending on where you live. The lender should clearly state the total cost, repayment date, and what happens if a payment fails. If anything feels foggy, pause. Clarity is your friend.

How the Online Application Usually Works

Most online applications are built to be quick. You provide basic personal details, proof you earn income, and banking info for funding and repayment. Some lenders verify identity digitally, so you may upload a document or answer credit file questions. Then you review the agreement and accept it electronically. After approval, funds are commonly sent by e-transfer or direct deposit, depending on the lender. Timing varies, and your bank’s processing can be the real boss in the room. A friend once joked, “I got approved fast, but my bank moved like it was on a coffee break.” That happens. So, make them simple, so you spend less time stressing and more time solving the problem.

Costs, Fees, and What You’re Agreeing to

Payday loans in Canada usually charge a set fee per $100 borrowed, instead of an interest rate you see on a credit card statement. That fee can add up quickly, especially on larger amounts. Your province may cap the maximum cost, but “capped” does not mean “cheap.” Always look at the total you’ll repay, not just the amount you receive. Also, watch for side charges. A missed payment can trigger NSF fees from your bank and fees from the lender, depending on the contract. Some lenders may offer an extension or a payment plan, but that can still cost more overall. Read the repayment date twice, like you’re checking the stove is off before leaving home.

Smarter Ways to Use It So It Doesn’t Bite You

If you choose this option, use it for a specific, time-sensitive expense. Keep it tight. “Fix the car so I can get to work” is clearer than “I’m short this month.” Before you borrow, map the next paycheque on paper and mark what must be paid first. It also helps to look at alternatives, even if you decide against them. A line of credit, overdraft, a credit union small loan, or asking a biller for a short extension can cost less. Some employers offer pay advances, and some communities have support programs for essentials. No shame in checking. Money pressure is loud, and sometimes the best move is turning down the volume with a cheaper option.

If you do go ahead, borrow the smallest amount that fixes the immediate issue. Set a reminder for the repayment date, and leave a buffer in your account so one random pre-authorized charge doesn’t trip you up. The goal is relief today without regret on payday.…

An emergency fund acts as your financial cushion, a safety net ready to catch you when life throws curveballs. Whether medical expenses or unexpected job loss, this fund helps you navigate challenging times without derailing your finances. Start by saving at least three to six months’ worth of living expenses. It gives you enough breathing room during emergencies. Open a separate savings account dedicated solely to this purpose; keeping it separate makes it less tempting to dip into for non-emergencies. Aim for small, consistent contributions rather than waiting for windfalls. Consider automating these transfers each month. Treating your emergency fund like any other bill ensures that saving becomes part of your routine and not an afterthought. Before you know it, you’ll have built up a solid financial buffer against uncertainty.

An emergency fund acts as your financial cushion, a safety net ready to catch you when life throws curveballs. Whether medical expenses or unexpected job loss, this fund helps you navigate challenging times without derailing your finances. Start by saving at least three to six months’ worth of living expenses. It gives you enough breathing room during emergencies. Open a separate savings account dedicated solely to this purpose; keeping it separate makes it less tempting to dip into for non-emergencies. Aim for small, consistent contributions rather than waiting for windfalls. Consider automating these transfers each month. Treating your emergency fund like any other bill ensures that saving becomes part of your routine and not an afterthought. Before you know it, you’ll have built up a solid financial buffer against uncertainty.

When investing in precious metals, there are four main options: gold, silver, platinum, and palladium. Each metal has its own unique properties and market factors to consider. For example, gold is typically seen as a safe haven investment and is often used as a hedge against inflation. Conversely, silver is more volatile than gold, but it can also offer higher potential returns. Doing your research and determining which metals align with your investment goals and risk tolerance is essential. According to a source, the best way to decide which precious metal to invest in is to ask yourself your goals and then figure out which metal best meets those objectives.

When investing in precious metals, there are four main options: gold, silver, platinum, and palladium. Each metal has its own unique properties and market factors to consider. For example, gold is typically seen as a safe haven investment and is often used as a hedge against inflation. Conversely, silver is more volatile than gold, but it can also offer higher potential returns. Doing your research and determining which metals align with your investment goals and risk tolerance is essential. According to a source, the best way to decide which precious metal to invest in is to ask yourself your goals and then figure out which metal best meets those objectives.

Before refinancing your mortgage, you should crunch the numbers and ensure it will save you money in the long run. That means considering closing costs, prepayment penalties, taxes, and insurance. It also means understanding how long you intend to stay in the house and comparing different loan options to ensure you’re getting the best deal.

Before refinancing your mortgage, you should crunch the numbers and ensure it will save you money in the long run. That means considering closing costs, prepayment penalties, taxes, and insurance. It also means understanding how long you intend to stay in the house and comparing different loan options to ensure you’re getting the best deal. In order to qualify for a competitive interest rate when refinancing your mortgage, it’s essential to have a good

In order to qualify for a competitive interest rate when refinancing your mortgage, it’s essential to have a good

It’s essential to understand what you’re borrowing, whether it’s a student loan, car loan, or home mortgage. Be sure to ask questions so that you understand the interest rate, repayment terms, and any fees associated with the loan. It’s also important to know if the interest rate is fixed or variable.

It’s essential to understand what you’re borrowing, whether it’s a student loan, car loan, or home mortgage. Be sure to ask questions so that you understand the interest rate, repayment terms, and any fees associated with the loan. It’s also important to know if the interest rate is fixed or variable. It’s important to keep track of how much you’ve borrowed, as well as how much you still owe. This can help you stay on top of your loan and ensure you’re on track to repay it.

It’s important to keep track of how much you’ve borrowed, as well as how much you still owe. This can help you stay on top of your loan and ensure you’re on track to repay it.

Now is the time to sit down and take a look at your budget. Where can you cut back on expenses? Do you really need that gym membership? Can you cancel your cable subscription and watch TV for free with an antenna? There are many ways to save money, and now is the time to start doing it to have emergency funds.

Now is the time to sit down and take a look at your budget. Where can you cut back on expenses? Do you really need that gym membership? Can you cancel your cable subscription and watch TV for free with an antenna? There are many ways to save money, and now is the time to start doing it to have emergency funds.

Another common cause of low credit scores is high balances on your credit cards. This can be caused by many different things, such as overspending, unexpected medical bills, or simply living beyond your means.

Another common cause of low credit scores is high balances on your credit cards. This can be caused by many different things, such as overspending, unexpected medical bills, or simply living beyond your means. One common cause of having a low credit score is using too much of the available credit. This can be in the form of maxing out your credit cards or having a high balance relative to your credit limit. This behavior is often viewed as risky by lenders and can lead to a lower credit score.

One common cause of having a low credit score is using too much of the available credit. This can be in the form of maxing out your credit cards or having a high balance relative to your credit limit. This behavior is often viewed as risky by lenders and can lead to a lower credit score.

Home renovation costs have been rising over the past few years, so it is no surprise that many homeowners are looking to refinance their mortgages. When a person refinanced their home previously, they could get a lower interest rate and use those savings towards renovating or improving their home. For example, if you purchased your house five years ago for $400K, you will get about $0.17 on the dollar for your home equity (assuming you bought at a 70% LTV ratio or paid 20% down).

Home renovation costs have been rising over the past few years, so it is no surprise that many homeowners are looking to refinance their mortgages. When a person refinanced their home previously, they could get a lower interest rate and use those savings towards renovating or improving their home. For example, if you purchased your house five years ago for $400K, you will get about $0.17 on the dollar for your home equity (assuming you bought at a 70% LTV ratio or paid 20% down). You won’t believe how many people refinance their mortgages to consolidate debts. By utilizing the money they’re saving with a lower mortgage rate, people can apply what would have been their monthly payment to pay off credit cards or other debts.

You won’t believe how many people refinance their mortgages to consolidate debts. By utilizing the money they’re saving with a lower mortgage rate, people can apply what would have been their monthly payment to pay off credit cards or other debts.

Always look at how much money you have to part with to get bitcoins. Luckily, you need not buy an entire bitcoin at once. They are easily divisible, and you can buy them in small units. You should consider going this route if you are still not sure about fully getting into cryptocurrency.

Always look at how much money you have to part with to get bitcoins. Luckily, you need not buy an entire bitcoin at once. They are easily divisible, and you can buy them in small units. You should consider going this route if you are still not sure about fully getting into cryptocurrency.

Debt cancellation is usually aimed at settling overdue debt. This is done by paying the creditor a reduced sum of money compared to the original value of the debt. In general, creditors and governments consider debt cancellation or debt reduction measures when the consequences of the debt suffered by the debtor are so severe that debt relief is the only solution.

Debt cancellation is usually aimed at settling overdue debt. This is done by paying the creditor a reduced sum of money compared to the original value of the debt. In general, creditors and governments consider debt cancellation or debt reduction measures when the consequences of the debt suffered by the debtor are so severe that debt relief is the only solution. Debt relief is beneficial because the debtor can settle his debts and save money. A collective debt settlement firm earns money from fees, and financial institutions receive more money than if the indebted individual had stopped paying their loans or declared bankruptcy.

Debt relief is beneficial because the debtor can settle his debts and save money. A collective debt settlement firm earns money from fees, and financial institutions receive more money than if the indebted individual had stopped paying their loans or declared bankruptcy. The goal of any debt settlement plan is, of course, to reduce your debt amount. Any debt cancellation strategy is only good if it allows you to reduce your debt to an amount owing. For example, reducing your debt by 60% is only possible if the customer can pay the remaining 40%, either in one installment or over a specified period.

The goal of any debt settlement plan is, of course, to reduce your debt amount. Any debt cancellation strategy is only good if it allows you to reduce your debt to an amount owing. For example, reducing your debt by 60% is only possible if the customer can pay the remaining 40%, either in one installment or over a specified period.

by the

by the

When it comes to the years of experience, make sure that you hire someone who has been in this field for more than five years.

When it comes to the years of experience, make sure that you hire someone who has been in this field for more than five years.

It is important to know the type of investors that you want for your company. If you are looking for capital for your biotech company, then look for people who are interested in the industry. There are chances that people who are interested in investing in Biotech Company are professionals in the field.

It is important to know the type of investors that you want for your company. If you are looking for capital for your biotech company, then look for people who are interested in the industry. There are chances that people who are interested in investing in Biotech Company are professionals in the field. When looking for investors for a biotech company, it is obvious that you will be tempted to look for investors already in the field. However, it is still important to make sure that you look for other willing investors. There are still investors who are willing to invest in a new field that is outside their comfort zone.

When looking for investors for a biotech company, it is obvious that you will be tempted to look for investors already in the field. However, it is still important to make sure that you look for other willing investors. There are still investors who are willing to invest in a new field that is outside their comfort zone.

Proper record keeping forms a major pillar when it comes to business financial matters. Many business owners have taken record keeping for granted leading to a great mix up in understanding transactions within their organization. Good records always ensure that one can trace any transaction within the business no matter when it was done.

Proper record keeping forms a major pillar when it comes to business financial matters. Many business owners have taken record keeping for granted leading to a great mix up in understanding transactions within their organization. Good records always ensure that one can trace any transaction within the business no matter when it was done.

For the lending institution, a student is just a customer like any other. The security of the firm is the ability of the client to pay the loan. A bank identifies people they can trust with loan using the credit bureau rating. It is a database maintained by all lending companies and business.

For the lending institution, a student is just a customer like any other. The security of the firm is the ability of the client to pay the loan. A bank identifies people they can trust with loan using the credit bureau rating. It is a database maintained by all lending companies and business.